In Part 1 of this two-part post, I explained that, owing to its endogeneity and consequent vulnerability to what I call Recursive Collective Action Predicaments, monetized public capital must, if it is to be productively rather than merely speculatively deployed, be publicly managed, while privately intermediated capital may be privately managed.I then suggested that public management of public capital can be helpfully modeled and implemented as a central bank balance sheet and its associated operations. In this post I take up that task.

Public Control over Public Assets

On the Public Asset side of the Fed Balance Sheet, the most straightforward and non-‘disruptive’ upgrade will in a sense be ‘retro.’ It is to reinstate the Fed’s original role as a two-tiered public capital manager comprising both (a) at the ‘macro’ level, a Federal Reserve Board tasked with modulating monetized credit aggregates economy-wide, and (b) at the ‘micro’ level, Regional Federal Reserve Banks tasked with allocating public capital only productively, not speculatively, as befits that network of regional development banks which the Fed System’s second tier was originally meant to be.

We lost sight of both (a) the Fed Board’s top tier macro-modulatory, and (b) the Regional Fed’s bottom tier allocative, purposes in the decades preceding 2008. Not accidentally, this was also the period when ‘macroeconomics’ all but disappeared as ‘a thing’ in highbrow economics circles, during which the understandable methodological imperative to harmonize macro- and microeconomics was mistaken for an imperative simply to jettison macroeconomics in the name of microeconomics.

It is sound to demand harmonization – indeed, this is precisely what my demonstrations elsewhere of sound modulation’s dependence on sound allocation in effect show. But it is foolish – and amounts to junk science – to count the obliteration of B as the harmonization of A and B. For in this realm, to jettison B is the jettison A as well.

The Macroprudential Turn – that is, the revival of ‘macroprudential,’ or ‘systemic risk,’ regulation – since 2008 signals at least some appreciation that the macro-modulatory function both can be and must be discharged. That is a genuine advance upon Greenspanian quietism, but it is not enough.

The problem with the post-2008 Dodd-Frank macroprudential revival is that it will not work absent a complementary allocative revival. If you follow any of the business press, you might have noticed that (speculative) ‘capital’ market indices have equaled or surpassed past records in recent years, even as job quality in payment terms, and now a pandemic, have deprived these market heights of any ‘fundamental’ justification sounding in production rather than endogenous-money-fueled speculation. There is your most recent indicator of good modulation’s dependence on good allocation. The Greenspan Put has become the Powell Put. And unlike Greenspan, Jay Powell has no alternative until we get allocation right.

Hence, productive Regional Fed lending will have once again to take both of the forms it originally took. Those were and will once again be: (a) direct purchases of productive project-associated paper issued by local and regional ‘operating companies’ (producers and service-providers); and (b) indirect lending to operating companies through public and private sector community banks that fund lending not with deposits, but through Fed Discount Window lending. Both (a) and (b) will be conditioned ex ante on projects’ likelihood of being productive, not speculative.

We already ‘spread’ the Fed’s investment-relevant data-gathering and data-analysis functions this way. It’s why the Regional Feds all, in the words of my Research Assistant, ‘write papers and stuff.’ These papers are aptly oriented toward regional conditions over which the Regional Feds have jurisdiction. The problem is that they can be only so useful when provided in effect only for private sector financial institutions, for reasons noted above.

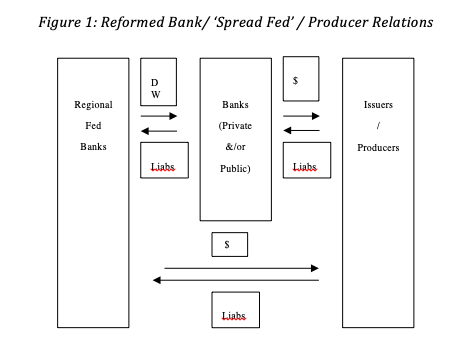

What we must do, then, is to reassign Regional Feds the tasks of lending (a) directly to local and regional enterprises through public purchase of private business paper, and (b) indirectly to the same through discount lending to community, public, and other local investment institutions. All such lending must be conditioned ex ante on planned projects’ promising to produce real goods and services, not yet more gambling or hedging opportunities, of which there are more than enough. Things would accordingly look as depicted in Figure 1, with ‘Liabs’ abbreviating ‘liabilities’ and ‘DW’ abbreviating ‘Fed Discount Window’:

Skeptics who claim that one ‘can’t really distinguish’ between productive and speculative investment at the margin must be dismissed with a smile. For one thing, most projected investments are not ‘marginal’ in this sense: their likely benefits well outstrip their up-front investment. In any event, we can err on the side of inclusion when times are tight and on the side of exclusion when things are overheating. For another thing, most Regional Fed research is into straightforwardly productive opportunities, not gambling opportunities – few if any institutions are better suited to spotting these than the Regional Feds.

Finally, the FSOC-inspired National Reconstruction and Development Council (NRDC) proposed below, which builds upon Professor Omarova’s and my earlier NIA proposal, will be a democratically accountable means of regularly determining and updating what counts as ‘development,’ hence ‘productive.’ Making and readily updating such determinations in the form of a ‘National Development Policy’ (NDP) is every bit as ‘existentially’ important as the Department of Defense’s formulation and regular updating of our Defense Posture Statement (DPS).

Redistributing Public Liabilities

Corresponding to the upgraded Public Asset side of the Fed’s Balance Sheet, of course, will be an upgraded Public Liability side of the same. Here the most straightforward measure will be to extend to all citizens, businesses, and legal residents of the nation a digital equivalent of the Federal Reserve Notes (paper dollars) and private sector bank Reserve Accounts that the Fed now issues and maintains. (We can think of these as digital wallet cousins of Ricks, Menand and Crawford, or Baradaran.) In other words, we add to Fed Liabilities here new liabilities of the same general type, just as we added to Fed Assets above new assets of the same general type. Abstracting from digitization, all that distinguishes the new from the old in both cases is their express public and productive, as distinguished from private and speculative, purposes.

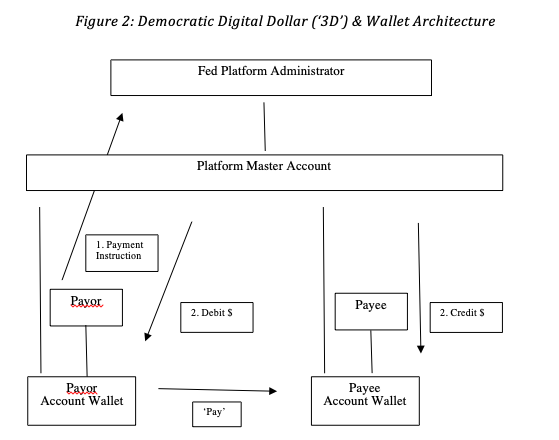

As for the ‘digital equivalent’ that I have in mind here, I refer simply to interest-bearing P2P digital wallets, the balances in which will be new Fed liabilities corresponding to the new Fed assets described at Step (7). This is my Democratic Digital Dollar (3D) and associated Fed Wallets proposal, which should be considered (a) the ‘end-game’ of my more immediately implementable Treasury Dollar and Digital Greenbacks proposals now before Congress, and (b) the national rendition of my state and municipal Inclusive Value Ledger (IVL) proposal now before the New York State Assembly and Senate as well as the Governor’s Office of New York and the Mayoral Office of Kansas City. The latter two measures could be taken this very autumn, with the first of them subsequently migrated to the Fed. Going this route would effectively recapitulate the history of the Treasury Greenback, which replaced unstable ‘wildcat banknotes’ – the paper predecessors of today’s welter of ‘crypto-currencies’ and other ‘digital assets’ – until the nation is ready to revive the Hamiltonian model of combined ‘central’-and-‘development’ banking, via the Federal Reserve Act, 50 years after the Greenback’s inception. That is the subject of my Money’s Past is Fintech’s Future work, also linked here. The upshot will look as depicted in Figure 2:

Private sector payments over the platform will occur on the liability side of the Fed balance sheet, just as accounts and payments now respectively subsist and occur on the liability sides of combined private sector bank balance sheets which themselves are in effect on the Fed balance sheet at one remove, via the banks’ own Reserve Accounts at the Fed. In effect, this will give perfect account-book reflection to the fact that, in trading with one another ‘severally’ in our private capacities, we are all trading liabilities that we ‘jointly’ issue – Fed promissory notes – in our public capacity.

Better Central Banking is Better Banking

Inasmuch as Federal Reserve Notes (paper dollars) and their fiduciary equivalent (Wicksellian bank money) are themselves Fed liabilities – indeed, our presently dominant form of monetized public capital instrument – the Democratic Digital Dollar will amount simply to (a) a digitization of already-existent Fed liabilities, and (b) a movement of the ‘bank money’ component thereof from private sector bank balance sheets to the Fed Balance Sheet. This will in turn make for far better banking than we presently enjoy.

It will make for far better banking in multiple ways: (a) There will be no more commercial or financial exclusion (that is ‘unbanked’ or ‘underbanked’ status) plaguing our citizenry or small businesses, nor will there be privately assessed rents known euphemistically as ‘fees.’ (b) There will be no more shortages of circulating payment media in isolated communities; and transaction speeds, hence growth, will accelerate. Justice and inclusion on the one hand, growth and efficiency on the other, thus combine to recommend this upgrade.

From a more instrumental, policy efficacy point of view, note that (c) monetary policy will no longer be subject to leakage owing to reliance on private sector financial institutions that ‘intermediate’ – that is, interfere with relations – between the citizenry and its central bank under this new arrangement. The Fed will modulate the national credit-money supply by raising and lowering interest paid out on wallets, not merely private sector bank interest on reserves (IOR). In extremis, it can even drop digital ‘helicopter money’ into citizens’ wallets. Improvements (a) through (c) are what we might label ‘core’ improvements to central banking, inasmuch as they speak to what central banking is meant to be for. There are also two collateral improvements that the upgraded Liability Side of the Fed Balance Sheet will bring, which are no less important for being ancillary: (d) Public authorities will be able to compensate currently uncompensated ‘care work’ upon digital ‘proof of work’ (POW). And finally (e), the 3D being a public commercial utility (as FedWire and FedNow are now), profits are removed from the picture while 4th Amendment protections are added – there will be no more breaches of commercial privacy or ‘harvesting’ of consumer financial data.

Collective Investment, Shared Return on Investment

We can round out the Capital Commons, Citizens’ Finance, or productive public capital picture with several complementary measures. First is an organizational tweak to our existing system of cabinet-level executive agencies that exercise jurisdiction over the nation’s infrastructure and industry: My proposed National Reconstruction & Development Council (NRDC) will be an ‘FSOC for National Development’ comprising the heads of all of the aforementioned cabinet level executive agencies.

As noted in passing above, the NRDC will develop, regularly update, and execute a National Development Policy (NDP), which is at least as important to long-term national security as is the National Defense Posture Statement (DPS) regularly updated by the Department of Defense (DOD). In so doing, the NRDC will both (a) afford guidance as to what we democratically deem ‘productive’ for purposes of Fed lending, and (b) coordinate with the Fed and Treasury, both of whose heads will sit on it just as they sit now on FSOC, in assuring that productive lending and national development occur evenly and equitably throughout our continent-spanning Republic in manners that are neither inflationary nor deflationary.

Finally, we can supplement our public capital management upgrade, should we wish, with equitable growth sharing and macroprudential price stabilization – my Citizen Growth Dividends proposal for regular UBI-like deposits into the Fed Wallets as national wealth grows as mentioned above, and my People’s Portfolio proposal characterized below. As to the former, there seems no reason for citizens not to share equitably in national economic growth financed with their public capital.

To be sure, some growth is attributable to the brilliance or diligence of inventors and entrepreneurs, and it is fine for our goods and services markets to reward them accordingly. But is sheer fantasy to believe (a) that markets for goods and services as we find them reward all in proportion to their marginal product, or (b) that such a regime would even be ethically interesting. Such is the upshot of my Meta-Theory of Justice, Putting Distribution First, and Just Prices work. Add to this the fact that growing effective demand in tandem with goods and services production themselves is the ultimate in ‘automatic stabilizers,’ and you have all the reason in the world to convey to all citizens a pro rata share in national growth over time. The Fed Wallets laid out above are the perfect receptacle.

Residual Stabilization: A “People’s Portfolio”

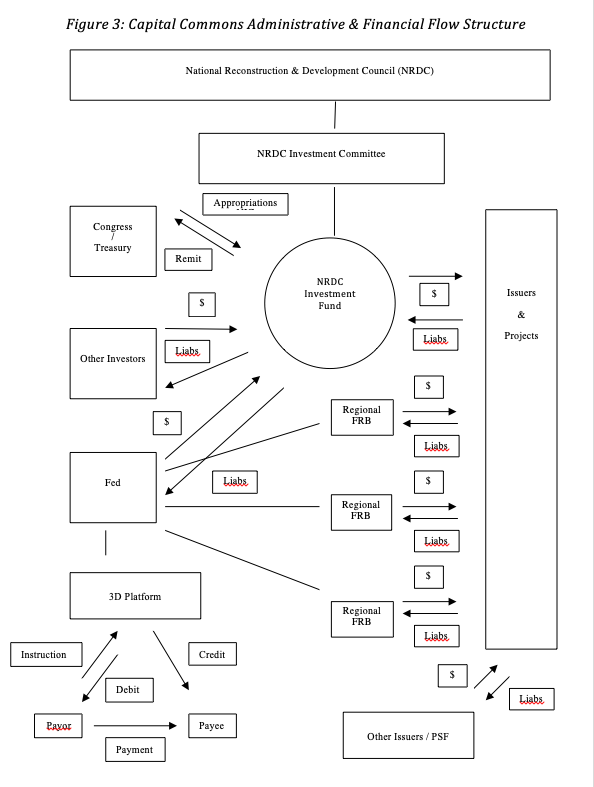

The Price Stabilization Fund (PSF), a.k.a. People’s Portfolio in Figure 3 below is for its part meant for open market operations to collar what I callSystemically Important Prices and Indices (SIPIs) – housing prices, fuel prices, Libor, some additional staple and commodity prices, and perhaps the SSP or prevailing wage rates at the bottom of the wage scale. The idea is to recognize that some such prices and indices of such prices are ‘systemically important’ in the same way as the Systemically Important Financial Institutions (SIFIs) that FSOC designates. These are prices that pervasively enter either directly into other prices as inputs, or indirectly into other prices by serving as benchmarks or reference points for other pricing decisions or derivative contracts.

The Fed has in effect long recognized at least one species of SIPI, and acted in the capital markets to ‘collar’ its movements within one narrow band – I refer to prevailing money rental, or ‘interest’ rates. Recent years have seen the Fed widen the sphere to include mortgage instruments and, now, even broad portfolios of corporate instruments – first in response to the dramas of 2006-09, and now in response to the Covid pandemic.

It is all but inevitable that the Fed, along with a new NRDC, will wish to target more such prices in future in the name of systemic financial stability. That will be partly because of effective credit-modulation’s practical dependence on good allocation as discussed above, and partly because ‘fine-tuning’ will be needed as the nation embarks next year on post-Covid reconstruction and then either a Green New Deal or a ‘Building Back Better’ revitalization of the kind also discussed above.

We can sum up the results of the foregoing in a single diagram as follows, in which connecting lines represent institutional relations and arrows represent financial flows.

Conclusion

Virtually everyone seems to agree that something’s gone wrong with our present financial arrangements – arrangements that sever public capital from publically cognizably productive investment. All appear likewise to agree that a national reconstruction, followed by serious national redevelopment, is now imperative. And now both the ideas of and the means to enabling public options for banking and even central bank-issued digital currencies are gaining traction as well.

Add in enthusiasm for a Building Back Better or Green New Deal, and it grows difficult not to grow giddy at this ‘perfect storm’ of readiness to do all that needs doing on both the asset and liability sides of our public ledger. These things are all sure to happen if darker – or hotter – forces don’t tear down or burn up our Republic before we’ve arrived. For the logic that forces them on us is hard not to see once it’s been pointed out, especially as the dysfunctions that this logic shows to be inevitable until we do it continue to gather all round us.