This post is part of a symposium on Jason Jackson’s Traders, Speculators, and Captains of Industry. Read the rest of the posts here.

** ** **

Jason Jackson’s erudite Traders, Speculators, and Captains of Industry tackles the question of how to understand India’s evolving foreign investment policy. Decisions about whether to promote domestic or foreign capital, he argues, have been guided by whether policymakers perceived the firm (be it Indian or foreign) as “traditional” or “modern.” Over a period spanning more than 100 years, what falls under these classifications changes. But Jackson demonstrates that the categories, and their influence, are remarkably persistent: perceptions of “traditional” capital attract policy hostility, while those of “modernity” court favorable treatment. It is also implicit in the book that we are speaking of large firms rather than what is known in India as MSMEs (micro, small, and medium enterprises).

The question that I want to pose—alluded to in Jackson’s suggestive conclusion—is how we should understand the modernity of so-called “modern Indian capitalists”? As Nasir Tyabji has influentially shown, the attempt to forge modern industrial capitalists out of businessmen during the Nehruvian era (1947-64) failed. This was, in part, because Indian capital never shed its identity as speculators and traders. Investment in capital goods creation, a central focus of the Five-Year Plans, was led primarily by the public sector. To the private sector, foreign exchange was rationed selectively, and foreign investment was generally limited to companies becoming junior partners in joint ventures. In this environment, politically well-connected firms who managed to get licensed began to benefit from a large and growing, protected internal market. They had limited incentives to innovate or seek overseas markets. To take just one example, the passenger automobile sector did not produce and sell new models between the 1960s and 1980s, and the original prototype and know-how for the models on the market had come from agreements with foreign partners.

Thirty-five years after the liberalization of the Indian economy, the pattern remains. And the stakes have perhaps never been greater, as a lack of innovation has prevented India from ascending the global value chain. The proportion of GDP coming from manufacturing is roughly the same as it was over a decade ago, and domestic firms have been unable to create world-class goods for internal and external consumption. Exceptions to this rule, including IT services, pharmaceuticals, gems and jewelry, are generally areas in which there are substantial labor cost advantages. Although a cumbersome regulatory environment and inadequate state investment may bear some responsibility for this state of affairs, we must also consider Indian firms’ reluctance to pursue substantial capital expenditures over longer time horizons or submit to transparent forms of corporate governance.

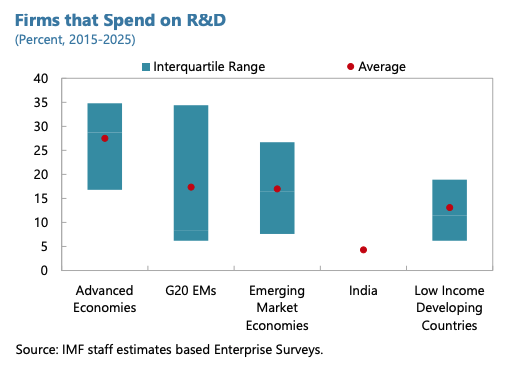

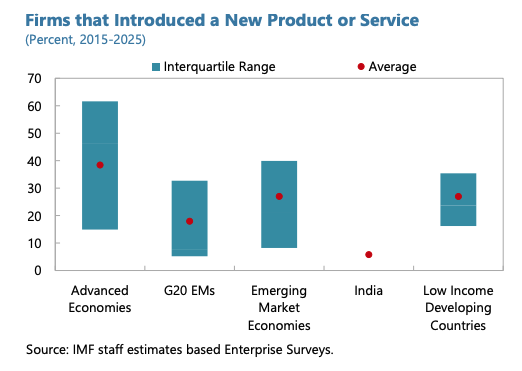

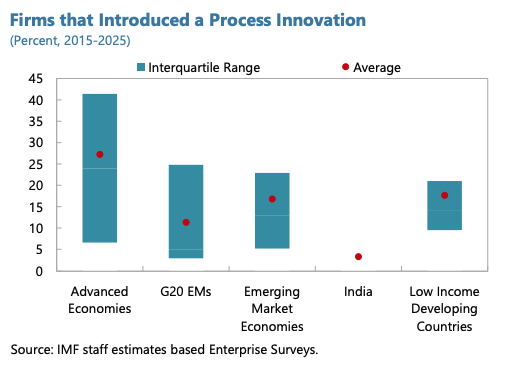

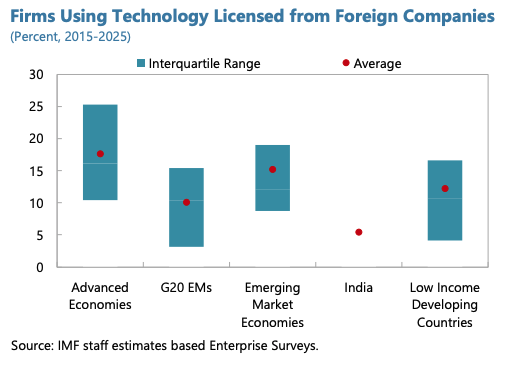

A few recent events and findings corroborate this stance. Consider the latest staff report on India by the IMF:

These tables are deeply revealing. Indian companies spend virtually nothing on R&D. They also clearly do not prioritize introducing new services or process innovations. To add insult to injury, neither do they manage to employ foreign technology via licensing. For all that firms profess interest in innovation, where they put their money tells a different story. Whereas public sector infrastructure investment has ramped up over the last decade, with the objective of crowding in private sector investment, the latter is still found wanting.

Another prominent issue holding back Indian firms is weak, unprofessional corporate governance, often sustained by government support. In January 2023, the US investment firm Hindenburg alleged that offshore shell companies were being used to artificially inflate the prices of listed Adani group companies (involved in everything from coal mining, to running ports, to real estate) and to hide weak financials of a conglomerate that has seen stock prices skyrocket and pursued substantial debt-fuelled growth. While the Indian government cleared Adani’s name, the move was widely understood as reflecting the group’s cosy relationship to political power.

To take another example, India’s behemoth conglomerate Tata Sons is dominated by the Tata Trusts, which enjoys a 65% ownership stake. The trusts have historically been controlled by the Tata family and its associates. Trust control led to the ousting of Cyrus Mistry, the first non-Tata CEO in its history, after he tried to shed lossmaking prestige acquisitions of his predecessor Ratan Tata. More recently, a controversy broke out between two factions of the trust, one led by the Chairman of the Trusts Noel Tata, and the other led by Cyrus Mistry’s cousin, Mehli Mistry. The disagreement centered on board representation at Tata Sons ahead of a vote on whether to pursue an IPO and subject the company to the rules and regulations of the stock exchange. Mistry was for listing, as the sale of Tata stock would have helped his ailing family business, which owned a major stake in Tata Sons. Noel Tata was opposed, as unlisted status carries much less oversight. In the end, the government sought to mediate between the two parties; Mistry quit. Tata Sons remains unlisted and has managed to extend the timeline given by the government to do so by September 30, 2025. To the extent that maximizing shareholder value is a motivation of a modern company, these practices do not seem to advance such objectives.

The bottom line is that Indian firms find ways to circumvent regulation to engage in speculation in what remains a well-protected and large domestic market. The ambitions of the “captains of industry” will continue to be in rent-seeking, controlling scarce resources auctioned by the government, and capturing larger market share for low value-added products to the domestic market. The symbiotic relationship between governments in power and Indian capital (now and in the past) means that there is perhaps little to nudge us away from this equilibrium. Their inability to engage in innovation or obey basic regulatory dictates should make us seriously question what ascribing a label of “modern” actually means.

I would like to suggest, then, that conceptualising Indian enterprise as already modern becomes a convenient way to block foreign competition or to lionize corporate barons, but that its correspondence to reality is thin. Jackson’s book helps us understand the varying ways in which this classification has provided great utility to the ones deploying it.